Introduction to Palo Alto Networks

Palo Alto Networks, Inc. (NASDAQ: PANW) stands as a cornerstone in the cybersecurity industry. Headquartered in Santa Clara, California, the company delivers cutting-edge solutions. These include next-generation firewalls and cloud security platforms.

The firm serves over 80,000 enterprise customers globally. This includes major corporations and government entities. Founded in 2005, it has grown into a leader amid rising digital threats.

As of November 22, 2025, the Palo Alto share price hovers around $183.16. This follows recent trading sessions with a daily range of $180.05 to $186.75. The stock’s market cap reaches approximately $125.07 billion.

Investors eye the Palo Alto share price for its alignment with tech sector expansion. Cybersecurity spending is projected to hit $366 billion by 2028. Palo Alto’s focus on AI-integrated defenses positions it well.

Company Overview and Core Offerings

Palo Alto Networks operates through three main platforms. Strata handles network security. Prisma secures cloud environments. Cortex manages security operations.

These platforms integrate to form a unified ecosystem. This approach reduces complexity for users. It also enhances threat detection via AI.

The company’s revenue model relies on subscriptions and services. Hardware sales complement these recurring streams. In fiscal 2025, total revenue hit $9.22 billion, up 14.87% year-over-year.

Net retention rates exceed 120%. This reflects strong customer loyalty and upsell success. Such metrics bolster confidence in the Palo Alto share price.

Historical Performance of Palo Alto Share Price

Since its 2012 IPO at about $8 per share (split-adjusted), the stock has surged. It delivered over 30% compound annual growth. Key drivers include demand for advanced security.

In 2020, amid the pandemic, shares jumped from $180 to over $400. Remote work amplified cyber risks. This period highlighted the stock’s resilience.

A 2023 dip below $150 came from inflation pressures. Recovery followed in 2024 with AI product launches. Year-to-date in 2025, gains reached 21% through early November.

The 52-week range spans from recent lows to a high of $221.38 on October 28, 2025. Volatility ties to earnings cycles and market sentiment.

Long-term returns average 25% annually. Share buybacks, like the $1 billion program through 2026, aid stability.

Key Milestones in Stock History

The 2012 debut marked entry into public markets. Early growth stemmed from firewall innovations.

By 2015, acquisitions like Cyvera boosted endpoint capabilities. This expanded the product suite.

The 2018 Evident.io buy laid Prisma Cloud’s foundation. Cloud security became a growth engine.

Pandemic-era surges in 2020 validated the platform model. Revenue diversification proved effective.

Recent years saw AI integrations. Prisma AIRS launch in 2024 drove rebounds.

These milestones correlate with Palo Alto share price uptrends. They underscore innovation’s role.

Recent Financial Results from Q1 FY2026

On November 19, 2025, Palo Alto reported Q1 FY2026 results. Revenue reached $2.47 billion, up 16% year-over-year. This beat estimates of $2.46 billion.

Non-GAAP EPS hit $0.93, exceeding forecasts of $0.89. Operating margin expanded to 30.2%. This topped the expected 29.1%.

Next-generation security ARR grew 29% to $5.9 billion. Remaining performance obligations rose 24% to $15.5 billion.

Adjusted free cash flow was $1.71 billion. Margins stood at 69.2%, up 17% from last year.

Guidance for Q2 includes $2.57-$2.59 billion in revenue. Full-year EPS projects $3.80-$3.90.

These beats support the Palo Alto share price premium. Yet, post-earnings dips reflect growth deceleration concerns.

Breakdown of Revenue Streams

Subscription revenue dominates at over 80% of total. This includes software and support.

Product revenue, from hardware, grew modestly. It contributes to initial deployments.

Services like professional help add stability. They ensure implementation success.

Geographically, Americas lead with 50% share. EMEA and APAC follow closely.

Platformization drives 30% year-over-year growth in adoptions. This shifts customers to integrated solutions.

Such diversification mitigates risks. It sustains Palo Alto share price momentum.

Factors Driving Current Palo Alto Share Price

Escalating cyber threats fuel demand. A 40-fold rise in attacks on portals since mid-November 2025 highlights urgency.

AI integrations, like Prisma AIRS 2.0, address new vulnerabilities. Partnerships with IBM and ServiceNow enhance appeal.

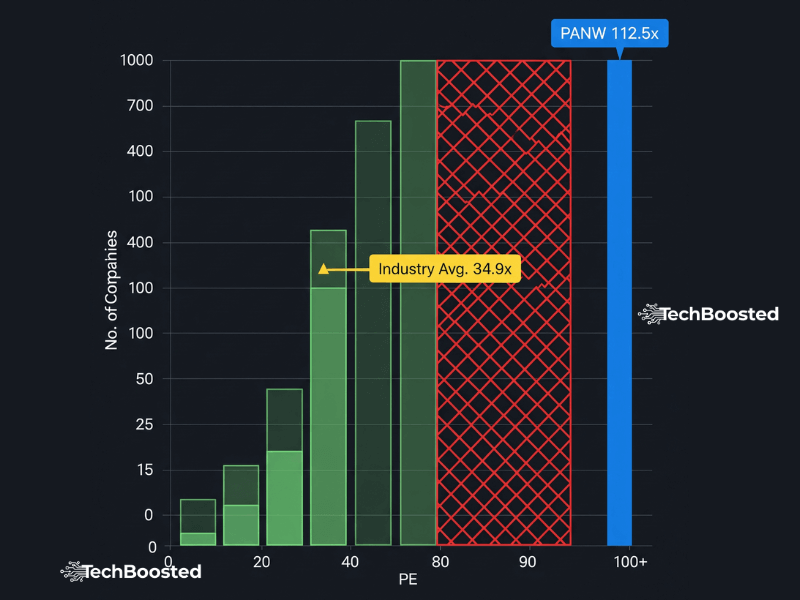

Valuation multiples, at 136.8x trailing P/E, draw scrutiny. HSBC’s recent “Reduce” rating cites a 2.3x PEG ratio.

Macro factors, including interest rates, add volatility. Tech rotations impact sentiment.

Acquisitions expand total addressable market. The Chronosphere deal targets observability.

Analyst upgrades, like BTIG’s $248 target, counterbalance cautions. Overall, positives outweigh near-term pressures.

Impact of Macroeconomic Trends

Rising interest rates pressure growth stocks. Palo Alto’s beta of 0.95 offers some insulation.

Inflation squeezes IT budgets. Yet, security remains a priority spend.

Geopolitical tensions boost cyber risks. This indirectly lifts Palo Alto share price.

Supply chain disruptions affect hardware. Subscriptions provide a buffer.

Global digital transformation sustains tailwinds. Cloud migrations favor Prisma.

Competitive Landscape Overview

Palo Alto leads in next-gen firewalls per Gartner. It holds about 0.11% network security share.

Fortinet competes on integrated, cost-effective solutions. Cisco leverages networking bundles.

Check Point focuses on prevention tech. Zscaler targets zero-trust cloud access.

CrowdStrike excels in endpoint detection. Emerging players like SonicWall eye SMBs.

Palo Alto’s platform unity yields 120% retention. This edges out siloed rivals.

Market position fortifies against erosion. AI and quantum initiatives maintain edge.

Market Share Analysis

In firewalls, Palo Alto claims top Gartner quadrant spot. Cloud security sees strong Prisma adoption.

Overall cybersecurity market fragments. Palo Alto captures via consolidation.

Competitors like Cloudflare dominate edges at 95.90% in some niches. Palo Alto broadens via acquisitions.

RPO growth to $15.5 billion signals share gains. Operating margins of 28.5% reflect efficiency.

This positioning supports Palo Alto share price resilience. Leadership in unified security prevails.

Analyst Ratings Breakdown

Consensus tilts “Strong Buy” from 42 analysts. Average 12-month target is $222.44.

Recent hikes include Jefferies to $250. Stephens raised to $215 with “Equal Weight.”

BMO Capital holds “Outperform” at $230. Cantor Fitzgerald stays “Overweight” at $250.

Cautions persist; Guggenheim’s “Sell” at $135 flags sustainability.

High targets reach $255; lows $135. Median $225 implies 23% upside from $183.

These views guide Palo Alto share price expectations. Bullish tilt dominates.

Price Target Projections

Short-term targets cluster around $220-$230. They factor Q1 beats and guidance.

Longer views eye $240+ by mid-2026. AI expansions underpin optimism.

Bear cases cap at $157 per HSBC. They stress valuation risks.

Upside scenarios hit $255 on ARR acceleration. Acquisitions like Chronosphere add catalysts.

Varied forecasts reflect polarized sentiment. Yet, 40 “Buy” ratings prevail.

Strategic Acquisitions in 2025

Palo Alto announced Chronosphere acquisition on November 19, 2025. Valued at $3.35 billion, it enters observability.

The deal closes in H2 FY2026. It adds $160 million ARR, growing triple-digits.

Earlier, Protect AI joined in July 2025 for $650-700 million. This bolsters AI model security.

IBM QRadar assets acquired in September 2024 for $1.14 billion. They enhance Cortex XSIAM.

CyberArk deal, at $25 billion in July 2025, targets identity security. It addresses AI cycles.

These moves expand TAM. They positively influence Palo Alto share price.

Future Outlook for Palo Alto Share Price

Projections see average $222.50 by late 2025. This marks 21% gain from current levels.

By 2026, estimates average $223. Some models forecast $592, though conservative at $208.

Bullish paths rely on Chronosphere integration. ARR could hit $20 billion by FY2030.

EPS CAGR of 17% supports growth. AI-native remediation via Cortex drives value.

Bear risks include delays and competition. Macro headwinds may slow to 14% annual growth.

DCF values at $235, 28% above now. “Year of the Defender” narrative aids.

Long-Term Predictions

Through 2029, Traders Union eyes $1,191. This assumes sustained innovation.

By 2030, averages near $1,092. Highs could reach $1,181 on market penetration.

Quantum-safe tech partnerships loom large. They future-proof offerings.

Global threats ensure demand. Platform expansions consolidate spending.

Volatility persists, but fundamentals shine. Palo Alto share price favors long holds.

Risks and Challenges Ahead

Execution on acquisitions poses hurdles. Integration costs could pressure margins.

Competition intensifies in AI security. Rivals like CrowdStrike innovate rapidly.

Regulatory scrutiny on data privacy grows. Quantum transitions add complexity.

Economic slowdowns curb budgets. High multiples invite corrections.

Geopolitical events spike threats but unsettle markets. Balanced portfolios mitigate.

Conclusion

Palo Alto Networks exemplifies cybersecurity leadership. Its platforms address evolving threats effectively.

Recent earnings and acquisitions signal strength. Despite volatility, growth prospects endure.

The Palo Alto share price reflects premium valuation. It rewards focus on innovation cycles.

Investors benefit from diversification. Long-term trends favor security stalwarts.

As AI reshapes risks, Palo Alto adapts swiftly. This positions shares for upside.

FAQs

What is the current Palo Alto share price?

As of November 22, 2025, the Palo Alto share price is $183.16.

How did Q1 FY2026 earnings impact the stock?

Revenue beat at $2.47 billion with EPS of $0.93. Shares dipped slightly post-announcement.

What is the latest acquisition by Palo Alto Networks?

Chronosphere for $3.35 billion, announced November 19, 2025, enhances observability.

What is the analyst consensus for Palo Alto shares?

Strong Buy rating with average target $222.44, implying 21% upside.

Who are Palo Alto’s primary competitors?

Fortinet, Cisco, Check Point, Zscaler, and CrowdStrike in key segments.

6. What is the 2026 price forecast for Palo Alto shares?

Averages around $223, with highs to $255 on growth catalysts.

Stay connected with TechBoosted for the latest updates on cybersecurity stocks and market analysis.